As part of its first Sustainability Report, and for the purposes of an ever-increasing desire to include its stakeholders, ICAB conducted its first materiality analysis, which identified the economic and governance, environmental and social issues most relevant to the company and its stakeholders. The process, with a view to continuous improvement, involved the participation of both ICAB employees and external stakeholders, and was essentially carried out in two main stages:

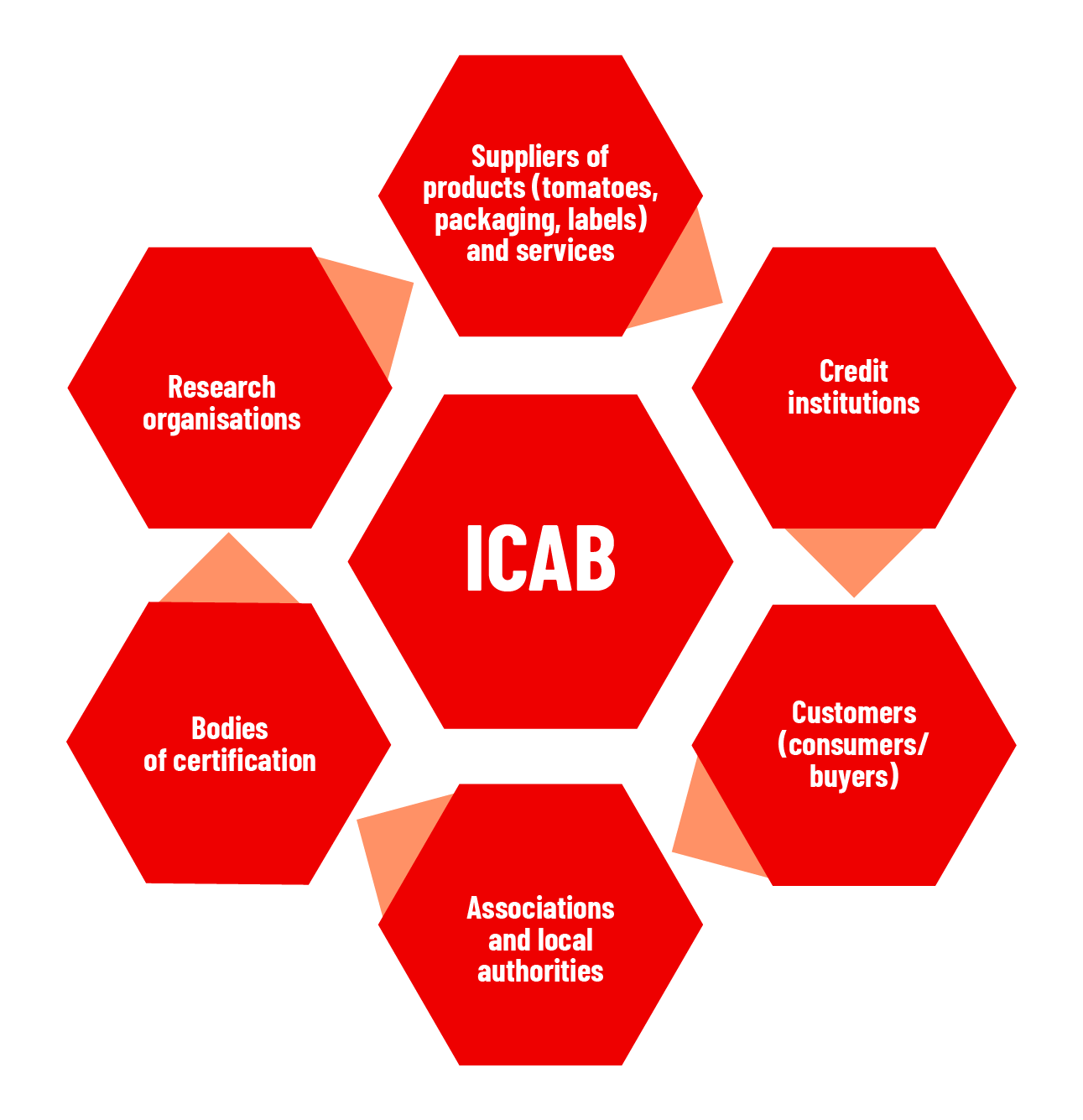

1. Initially, a Mapping the most important stakeholders for ICAB., sharing with them the stakeholder engagement questionnaire. This first moment of discussion allowed them to assess and define the material issues covered in this reporting through the expression of their preferences on the listed topics.

2. Secondly, some interviews With key corporate employees representing various functions such as Administration, HR, Quality Control, Raw Material Procurement, Supplier Management, Management Systems, with the purpose of analyzing the management methods, safeguards, initiated projects and future projects, risks and opportunities related to the material issues that emerged from the stakeholder engagement and thus validating what emerged from the questionnaire, as well as verifying such elements as the content, quality, completeness and accuracy of the Sustainability Report.

We felt it was essential to involve all of our stakeholders so as to gather as many instances and insights as possible, while remaining open to dialogue and needs for discussion.

The questionnaire revealed 26 responses broken down as follows:

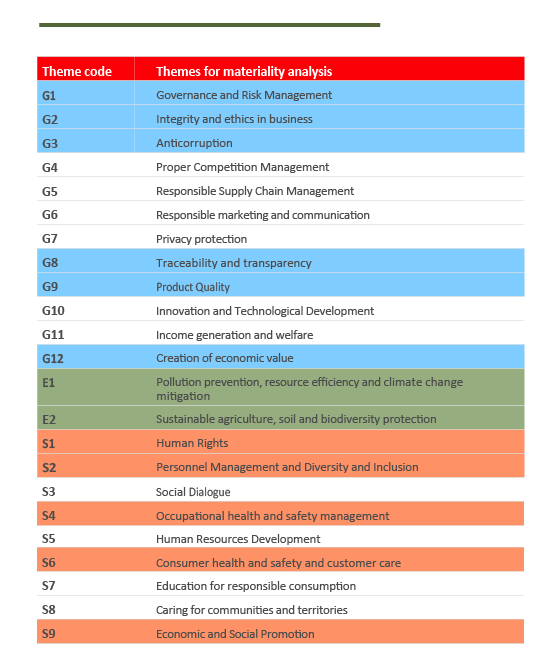

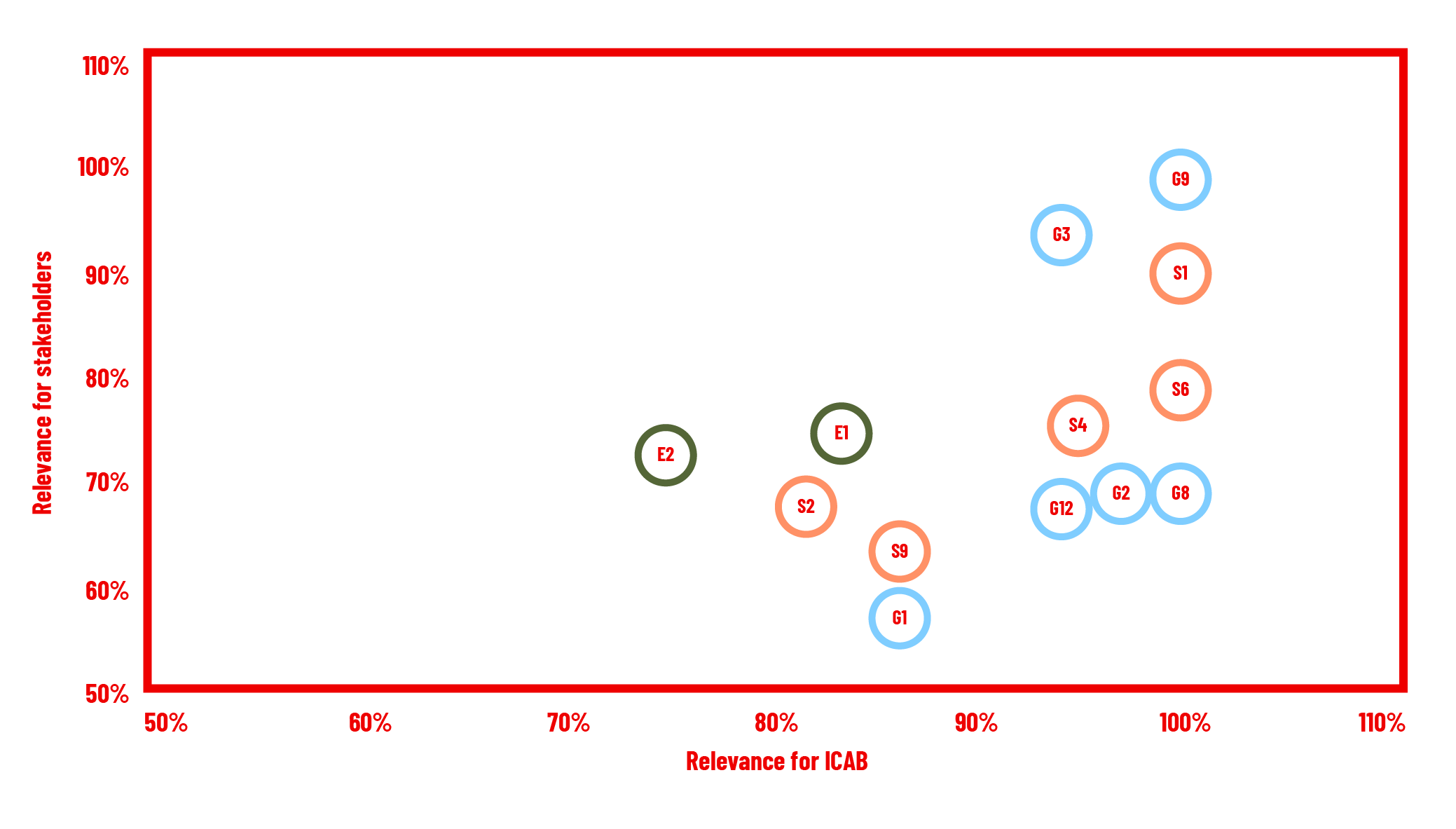

The stakeholder engagement process led to the identification of the following material issues, summarized in the materiality matrix. All three dimensions of sustainability (economic and governance, environmental, and social) were considered to be relevant to stakeholders, with a prominence of issues pertaining to the economic and governance spheres. The upper right portion of the matrix represents the selection of the most relevant, and therefore material, aspects for both ICAB (x-axis) and external stakeholders (y-axis). All issues included within the quadrant are those found to have a value at or above the materiality threshold as revealed during stakeholder engagement activities.